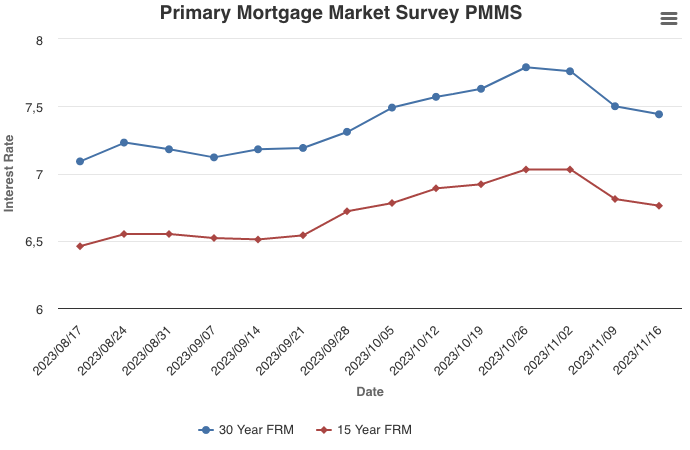

For Week Ending November 18, 2023

For Week Ending November 18, 2023

U.S. home seller profits continue to rise, with profit margins on median-priced single-family home and condo sales climbing to 59% in the third quarter of the year, up from 56.6% in the second quarter of 2023, according to ATTOM’s Q3 2023 U.S. Home Sales Report. Typical profit margins increased from the second quarter to the third quarter of 2023 in 85 of 155 metropolitan statistical areas analyzed, although profits were down year-over-year in 103, or 66%, of those metro areas.

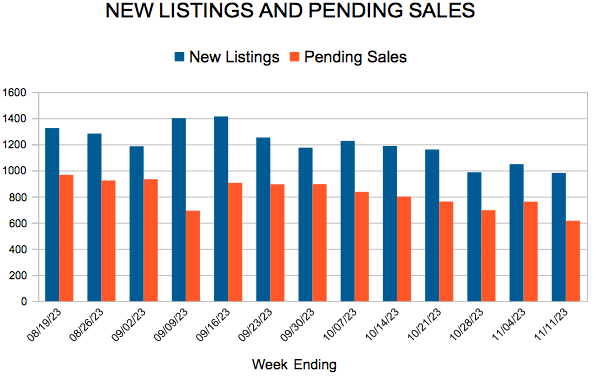

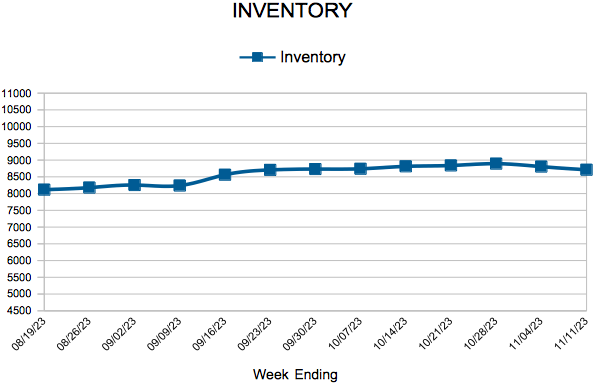

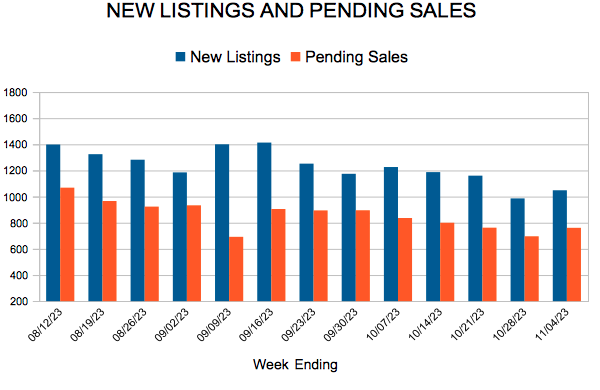

IN THE TWIN CITIES REGION, FOR THE WEEK ENDING NOVEMBER 18:

- New Listings decreased 5.9% to 934

- Pending Sales increased 3.6% to 711

- Inventory decreased 5.4% to 8,543

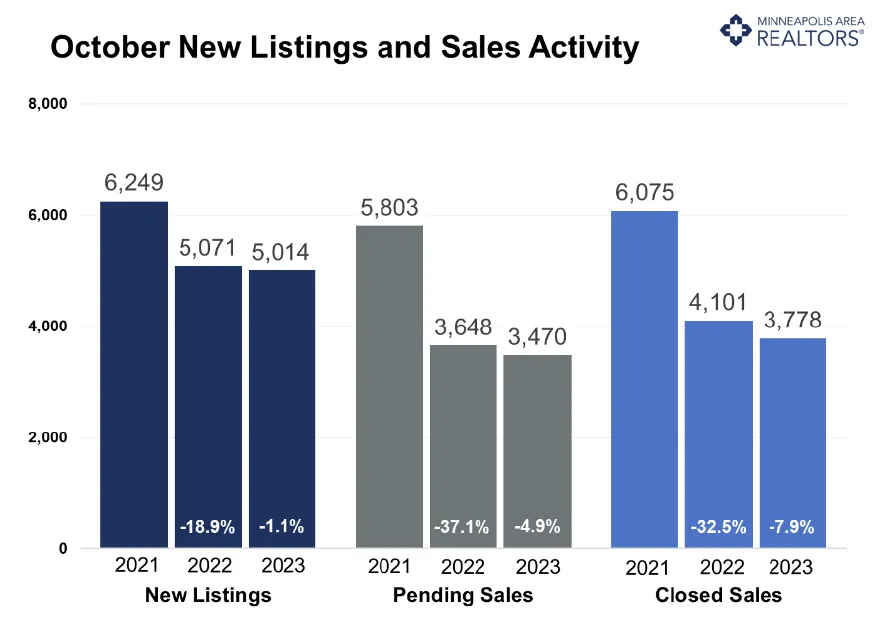

FOR THE MONTH OF OCTOBER:

- Median Sales Price increased 2.4% to $365,000

- Days on Market increased 2.8% to 37

- Percent of Original List Price Received increased 0.2% to 98.4%

- Months Supply of Homes For Sale increased 20.0% to 2.4

All comparisons are to 2022

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.