Inventory

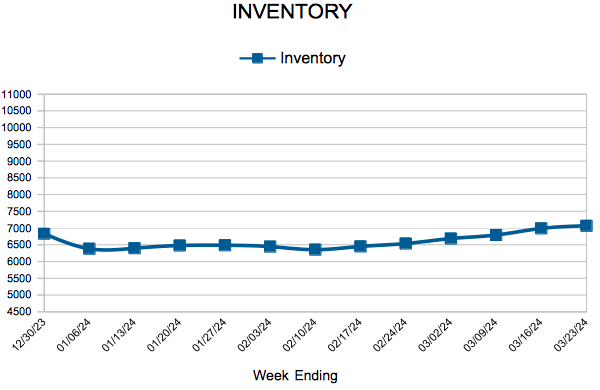

For Week Ending March 23, 2024

For Week Ending March 23, 2024

Housing inventory continues to improve nationwide, climbing 14.8% year-over-year according to Realtor.com’s February 2024 Monthly Housing Market Trends Report. New listings increased 11.3% year-over-year, while the total number of unsold homes rose 8.8% compared to the same period last year. Of particular note was the rise in inventory of homes in the $200,000 to $350,000 price range, which grew 20.6% annually, outpacing all other price categories.

IN THE TWIN CITIES REGION, FOR THE WEEK ENDING MARCH 23:

FOR THE MONTH OF FEBRUARY:

All comparisons are to 2023

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.

March 28, 2024

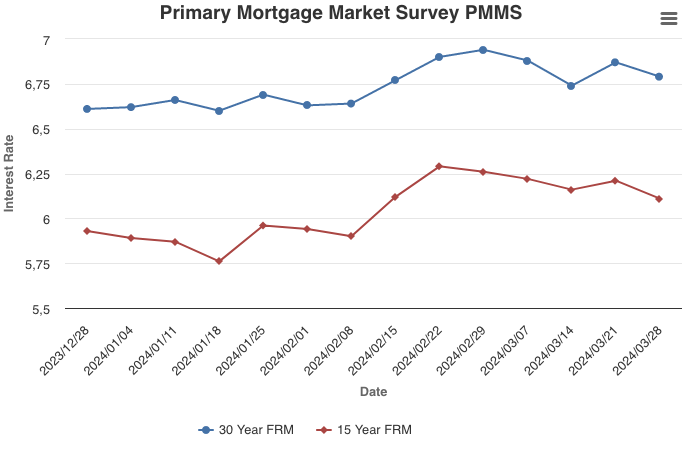

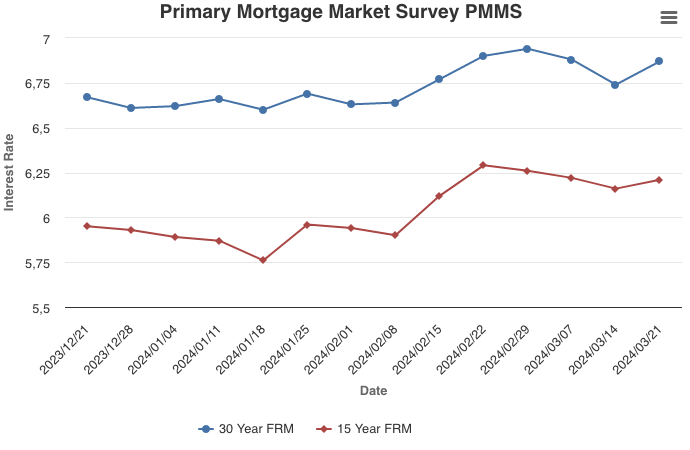

Mortgage rates moved slightly lower this week, providing a bit more room in the budgets of some prospective homebuyers. Additionally, encouraging data out on existing home sales reflects improving inventory. Regardless, rates remain elevated near seven percent as markets watch for signs of cooling inflation, hoping that rates will come down further.

Information provided by Freddie Mac.

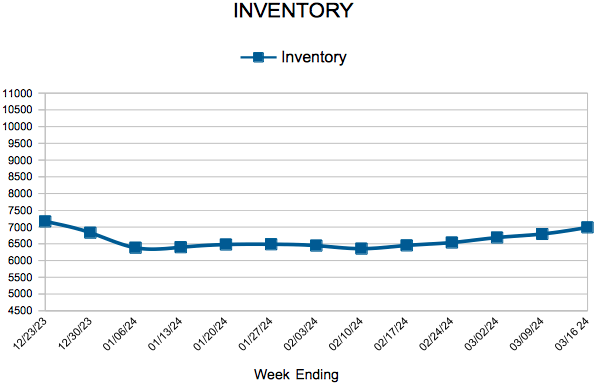

For Week Ending March 16, 2024

For Week Ending March 16, 2024

The U.S. homeownership rate declined in the fourth quarter of 2023, sliding 0.3% from the third quarter to 65.7% at year’s end, according to the Census Bureau’s Housing Vacancy Survey, as higher interest rates and a limited supply of inventory put homeownership out of reach for some buyers. The latest reading fell short of the 25-year average rate of 66.4%, with the less than 35 age group experiencing the largest quarterly decline in homeownership rate, at 0.6%.

IN THE TWIN CITIES REGION, FOR THE WEEK ENDING MARCH 16:

FOR THE MONTH OF FEBRUARY:

All comparisons are to 2023

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.

March 21, 2024

After decreasing for a couple of weeks, mortgage rates are once again on the upswing. As the spring homebuying season gets underway, existing home inventory has increased slightly and new home construction has picked up. Despite elevated rates, homebuilders are displaying renewed confidence in the housing market, focusing on the fact that there is a good amount of pent-up demand, an ongoing supply shortage and expectations that the Federal Reserve will cut rates later in the year.

Information provided by Freddie Mac.

(Mar. 18, 2024) – According to new data from Minneapolis Area REALTORS® and the Saint Paul Area Association of REALTORS®, both buyer and seller activity rose in February. Homes also sold in less time and at higher prices.

Sellers, Buyers and Housing Supply

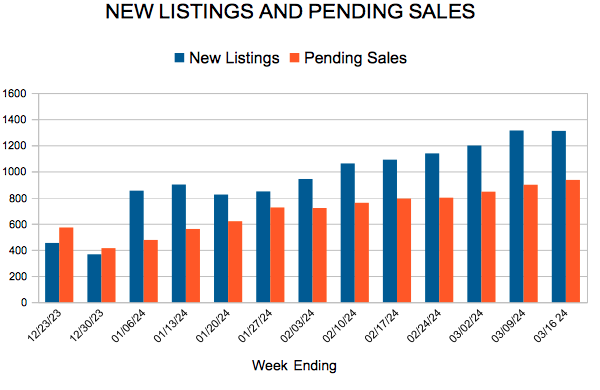

With four consecutive year-over-year increases in new listings and three consecutive year-over-year increases in pending sales, the market turnaround narrative is gaining traction. While inventory levels were up, potential buyers should understand that the market remains significantly undersupplied. In February, sellers listed 34.5% more homes on the market and buyers signed 13.1% more purchase agreements. Sellers unwilling to give up their favorable mortgage rate have withheld listings due to the “rate lock-in effect” but now there is a backlog and we’re seeing some of that activity being released. Buyers had also delayed their purchases until rates came down or until they had some earnings growth, were more able to save for a downpayment and saw more inventory that met their needs. While supply and demand normalize, buyer and seller activity won’t immediately return to previous highs. That will take time—but just how much depends on both market and economic factors. Since these seemingly strong gains are skewed by a low baseline period, it’s not that activity has surged recently as much as activity declined last year at this time due to the Federal Reserve’s inflation fight and rate hikes.

Inventory levels are on the rise in the metro, up 13.3% compared to last February. Those out shopping for homes during this spring market should expect both more listings from pent-up sellers but also more competition from pent-up buyers. In that sense, activity levels will be higher but the balance between supply and demand will remain tight. But if rates do fall further, that could induce even more demand which would cause a resurgence in multiple offer situations and homes selling for over list price. “Perhaps it’s still early to make the call, but it sure feels like we’ve reached a turning point,” said Jamar Hardy, President of Minneapolis Area REALTORS®. “Despite the market ramping up, buyers are still cautious and deliberate but also more optimistic.”

Prices, Market Times and Negotiations

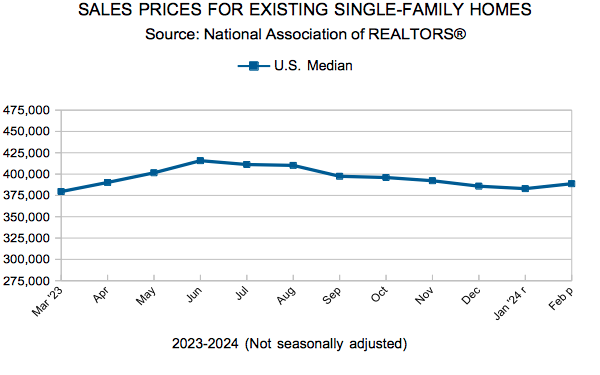

Supply levels are too low for prices to fall but rates are too high for prices to rise much. The median sales price rose 4.5% to $357,700, which amounted to $203 per square foot. During the month, sellers accepted offers at 97.5% of list price after 59 days compared to 97.2% in 61 days last February. Sellers still enjoy pricing power and the upper hand in general but some are having to make concessions by way of price reductions, some seller paid closing costs and other tactics. “There is definitely some momentum heading into spring market,” said Amy Peterson, President of the Saint Paul Area Association of REALTORS®. “But turnarounds rarely happen overnight. Builders play a key role, lenders are being more innovative and consumers are persistent and more realistic.”

Location & Property Type

Market activity always varies by area, price point and property type. New home sales rose at over twice the rate of existing home sales. Single family sales rose at over twice the rate as townhomes. Sales over $500,000 rose at over three times the rate of sales under $500,000. Cities such as Shorewood, Forest Lake, Minnetrista and New Richmond saw among the largest sales gains while Crystal, Andover, Buffalo and Inver Grove Heights all had notably weaker demand. For cities with at least five sales, the highest priced areas were Medina, Orono, North Oaks and Lake Elmo while the most affordable areas were Red Wing, Zumbrota and Vadnais Heights.

February 2024 Housing Takeaways (compared to a year ago)

Licensed In Minnesota

All information deemed reliable but not guaranteed and should be independently verified.