For Week Ending January 13, 2024

For Week Ending January 13, 2024

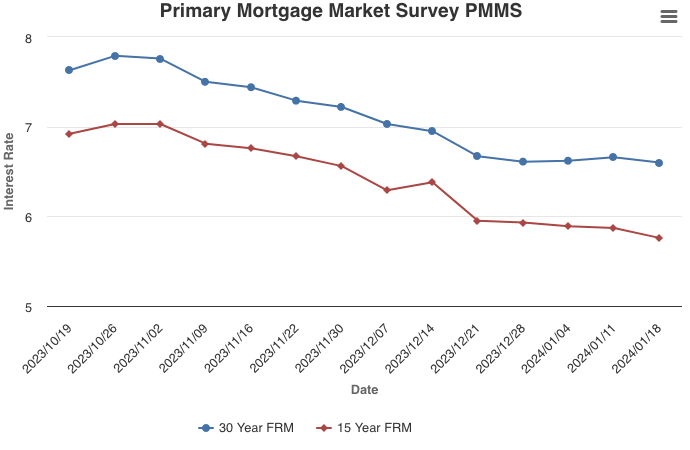

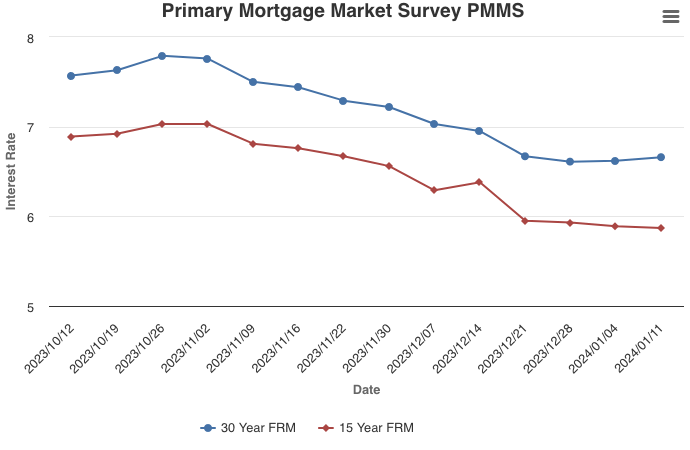

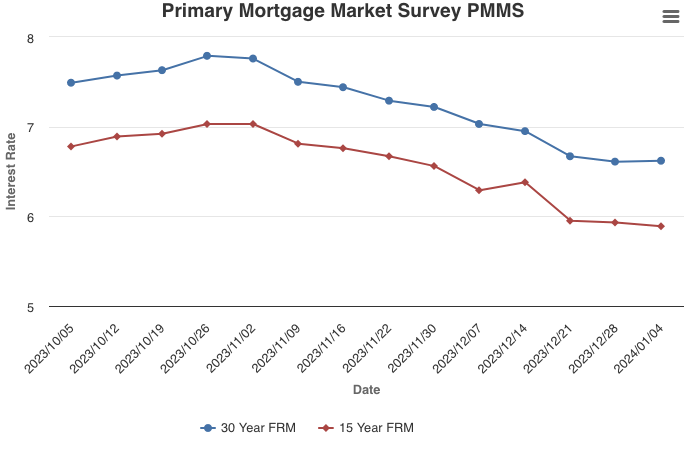

Fannie Mae’s Home Purchase Sentiment Index (HPSI) climbed nearly three points to 67.2 in December and was up 6.2 points year-over-year, according to the latest National Housing Survey®. The rise was attributed to increasing consumer optimism about mortgage rates, with a survey-high 31% of respondents indicating they expect mortgage rates will decline over the next 12 months. Homeowners, in particular, had greater optimism about the future of mortgage rates than renters, which could encourage some would-be sellers to list their homes this year, helping to increase the supply of existing homes for sale.

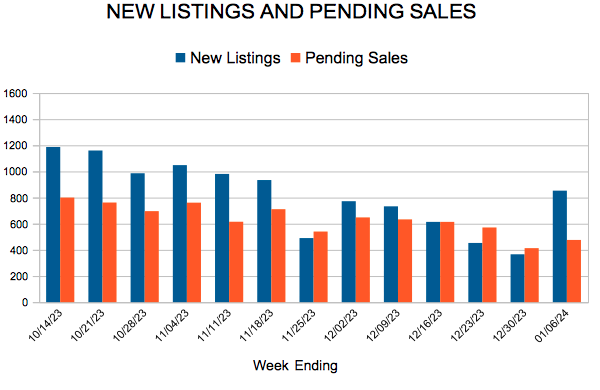

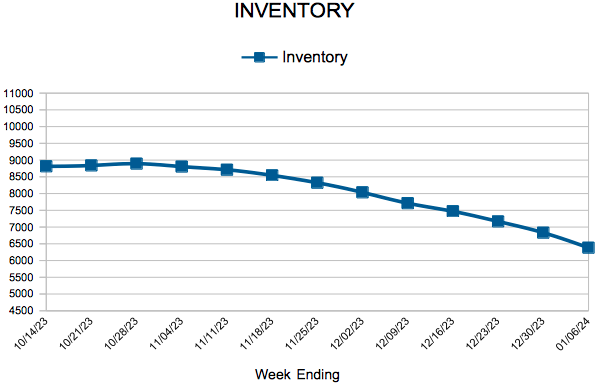

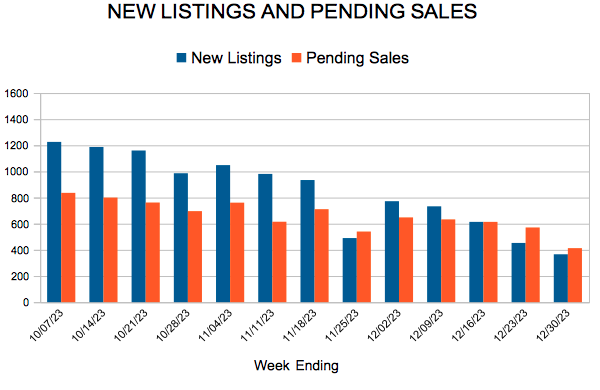

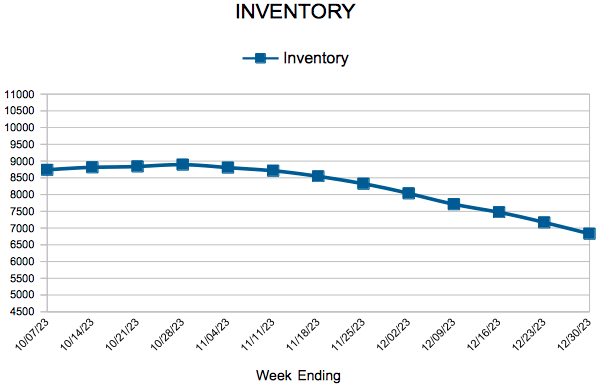

IN THE TWIN CITIES REGION, FOR THE WEEK ENDING JANUARY 13:

- New Listings increased 14.5% to 900

- Pending Sales increased 2.6% to 560

- Inventory decreased 4.2% to 6,397

FOR THE MONTH OF DECEMBER:

- Median Sales Price increased 1.3% to $353,700

- Days on Market remained flat at 50

- Percent of Original List Price Received increased 0.4% to 96.7%

- Months Supply of Homes For Sale increased 13.3% to 1.7

All comparisons are to 2023

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.